How to opt out of credit card offers

You can opt out of credit card offers by visiting optoutprescreen.com and submitting an opt-out request.

You have two options: to opt out for five years only or permanently. Both options are available online for free.

Updated: October 01, 2025

In short, to opt out:

- Go to www.optoutprescreen.com.

- Scroll down the page and select “click here to opt-in or opt-out.”

- Select the type of opt-out you want, fill out the form, and confirm your request.

Need some help?

See our detailed guide below.

Opt out of credit card offers: a step-by-step guide

Read on if you’re having any difficulty opting out from credit card offers.

We’ll provide clear instructions, together with screenshots, and necessary links.

Do not fill out this form on public computers or shared devices.

1. Go to www.optoutprescreen.com

- Open a new tab and type in www.optoutprescreen.com or click here.

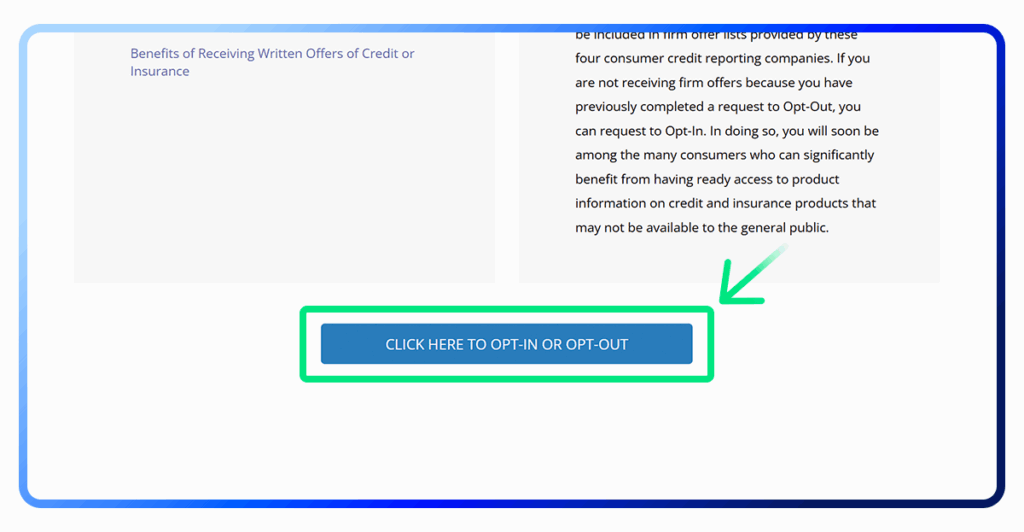

- Once the website loads, scroll down to the bottom of the page.

- Look for a button that says “click here to opt-in or opt-out” and click on it.

- You’ll be directed to a new page.

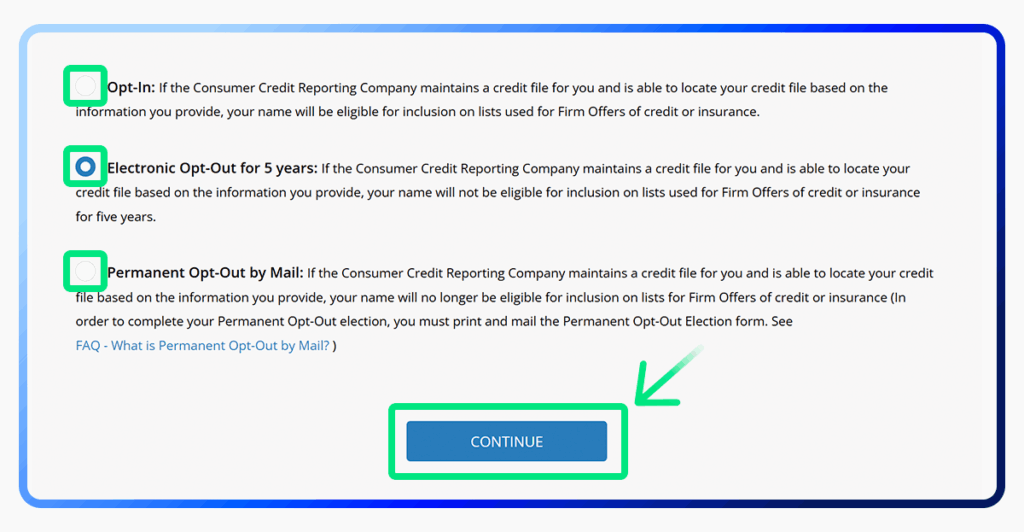

3. Select the type of opt-out you want and click “continue”

- You should see different options for opting out. Choose the one that best fits your needs by clicking the circle next to it.

- After making a selection, click the “continue” button to move to the next step.

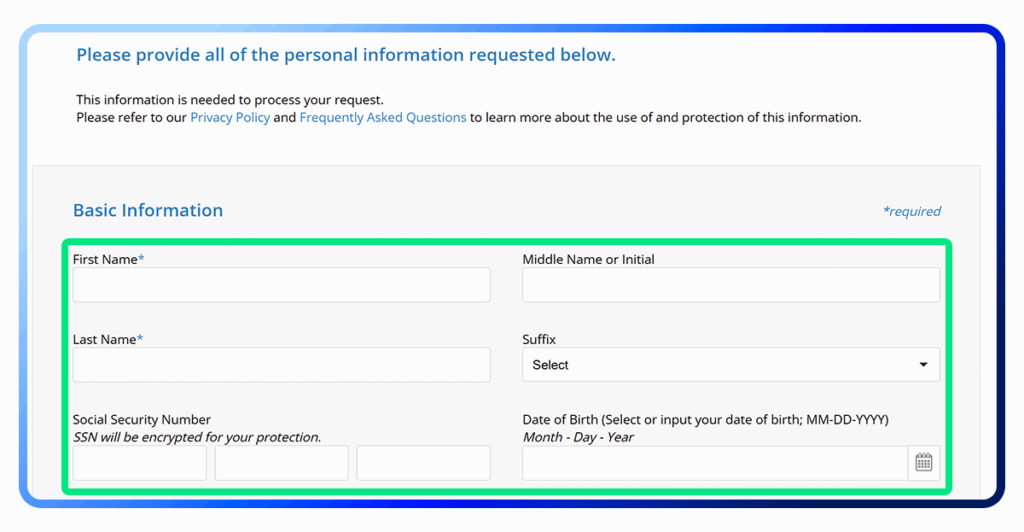

4. Fill out the opt-out form

- A form will appear on your screen. Carefully fill in all the required information.

- The form asks for some basic information, like your name and surname, but also for other, highly sensitive data, like your SSN.

- We recommend providing only the required information—marked with an asterisk (“*”). Your SSN is not required.

- Make sure all the information is correct before moving on.

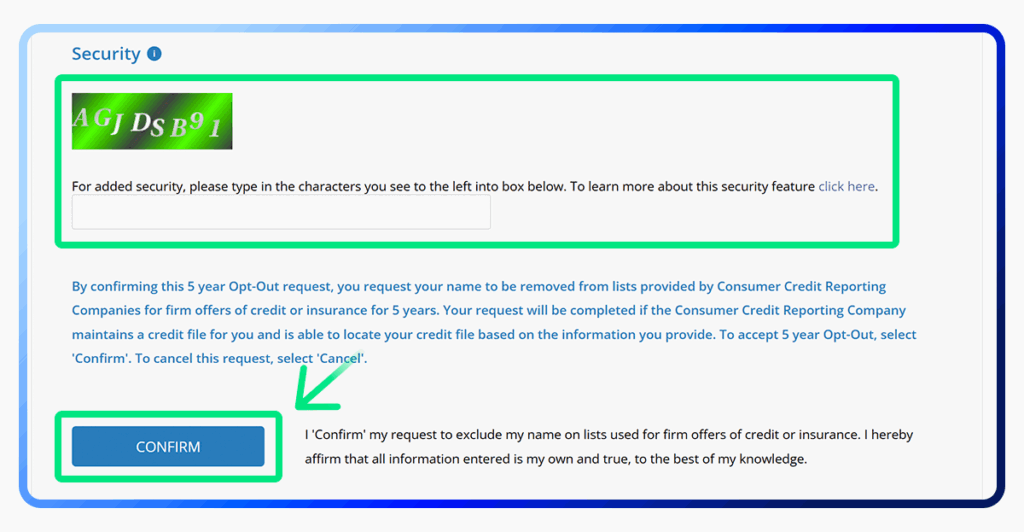

5. Enter the security code at the bottom and click “confirm”

- At the bottom of the form, you’ll see a security code. This is usually a series of letters and numbers.

- Type this code exactly as it appears into the box provided. This step is to ensure that you are a real person and not a computer program.

- Once you’ve entered the code, click the “confirm” button to complete the process.

Opt out from other offers and spam as well

Opting out of other marketing offers or spam messages may not be as simple as with credit cards, but there is still a way to do it.

You see, for anyone to send you an offer, they first need to know your contact information.

That information is usually bought from data brokers—companies that specialize in gathering your data and trading it with third parties.

But if data brokers don’t have your information, there’s nothing for them to trade.

Here’s how to do it:

- You can opt out of each data broker yourself → see our guide to learn more.

Or—

- Sign up to Incogni—a professional data removal service—to handle this for you.

Once you sign in, we’ll immediately send over 100 data removal requests to top data brokers.

And that’s just the beginning.

To keep your information secure, we’ll continue sending removal requests on a regular basis, ensuring your data doesn’t find its way back into brokers’ databases.

With our Family & Friends Plan, your loved ones are protected as well.

Don’t let companies use your personal data for their own benefit.

FAQ

Will opting out affect my credit score?

No, opting out of preselected credit card offers won’t change your credit score. Your credit score is based on your financial behavior, not on whether you receive these offers.

Will opting out stop all unwanted mail and phone calls?

No, opting out will only stop pre-screened offers from major credit bureaus. You’ll still get mail and calls from other sources like charities or alumni groups because they use different lists.

What is the Fair Credit Reporting Act?

The Fair Credit Reporting Act (FCRA) is a law that ensures fairness and privacy in how your credit information is used. It sets rules for how credit card companies can handle your personal data.

What are soft inquiries?

Soft inquiries, or soft credit checks, happen when a credit card company looks at your credit history to see if you qualify for pre-screened offers. These checks don’t affect your credit score.